This is the first post in a multi-part series, Insurance Foundations.

To understand what insurance is, it’s important to start with the basics. It’s hard to get more basic than this: what problem does insurance solve?

The answer is that insurance is one of several tools used for risk management. But it’s important to understand the scope of the phrase “risk management” when used like this. There are all sorts of risks out there — personal, reputational, legal, existential, and more. However, from a business and insurance standpoint, the phrase “risk management” refers specifically to financial risk. Financial risk is the possibility of suffering a financial loss because of circumstances outside your control.

Everyone faces financial risk throughout their entire lifetime. While the probability of a financial risk can be calculated, the exact details of timing, severity, and impact can’t be known until a loss actually happens. As a result, while it’s not possible to create a plan of action for a specific loss, it is possible — and, in fact, well-advised — to create and maintain a toolbox designed to mitigate potential risks.

That’s what risk management is all about. It’s often seen as a subfield of business finance, but more and more, it’s being recognized as a business field in its own right.

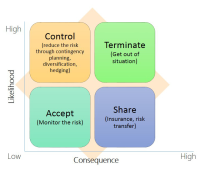

How is risk managed?

Image: Nirjal stha

Risk management practices are generally divided into four broad strategies:

- Risk avoidance involves avoiding any activity or situation that could cause a financial loss. That’s the technique being used when someone chooses not to participate in an activity they think is too dangerous; or when a business decides not to pursue a particular product because of concerns that it could cost more than they’d earn back in sales. The problem with risk avoidance is that, if all risks are avoided, so are all potential rewards. At some point, it’s necessary to take a chance on a potential loss. Risk avoidance is all about choosing which chances to take.

- Risk retention is the risk that someone chooses to take, knowing that there could be a potential cost. When a company launches a new product line, they can do market research to determine whether it might be successful, but they won’t know if it will be successful until they actually launch it. This same technique comes into play when it’s time to choose which car or house to purchase, or even the decision to own versus rent your home.

- Risk reduction (or mitigation) is taking steps to minimize or reduce the chances of a financial loss. The difference between this technique and risk avoidance is that, while risk reduction makes a loss less likely, it doesn’t avoid it altogether. This is the technique someone uses when they make sure their car is in good condition and their house soundly built. In the business world, risk reduction involves adding redundancies in production, security protocols when necessary, and periodic audits to make sure things aren’t getting off track and developing into a less-than-acceptable risk.

- Risk transfer, the final strategy, involves shifting some or all aspects of a risk to a third party. This is the technique you use when you choose to hire a professional instead of DIY’ing a repair, or when asking that professional for a warranty or work guarantee. Outsourcing business functions is another example of risk transfer; it shifts the operational risks to the outsourced company. But the most common risk transfer technique is purchasing insurance.

How does insurance fit in?

Insurance, then, is a subset of a broader risk management strategy. It is not designed to stand alone as the only method of risk management. In fact, in most circumstances, insurance coverage should be the last resort, used when other risk management practices prove insufficient. That’s because insurance only comes into play after a financial loss has occurred — it manages impact, not timing or severity.

In the next post, I’ll explain the primary concept behind insurance: risk pooling.